August 30, 2021

Don’t Forget About The Dividend | Important Investing Principle

Don’t forget about the dividend! This is one of the most important investing principles as dividends add value to a portfolio. They can provide a cushion for investors when growth of principal can be hard to come by, they can enhance total return over a long period of time by compounding reinvestments, and they can be the source of income for retirees who choose to live off the dividend rather than draw down principal.

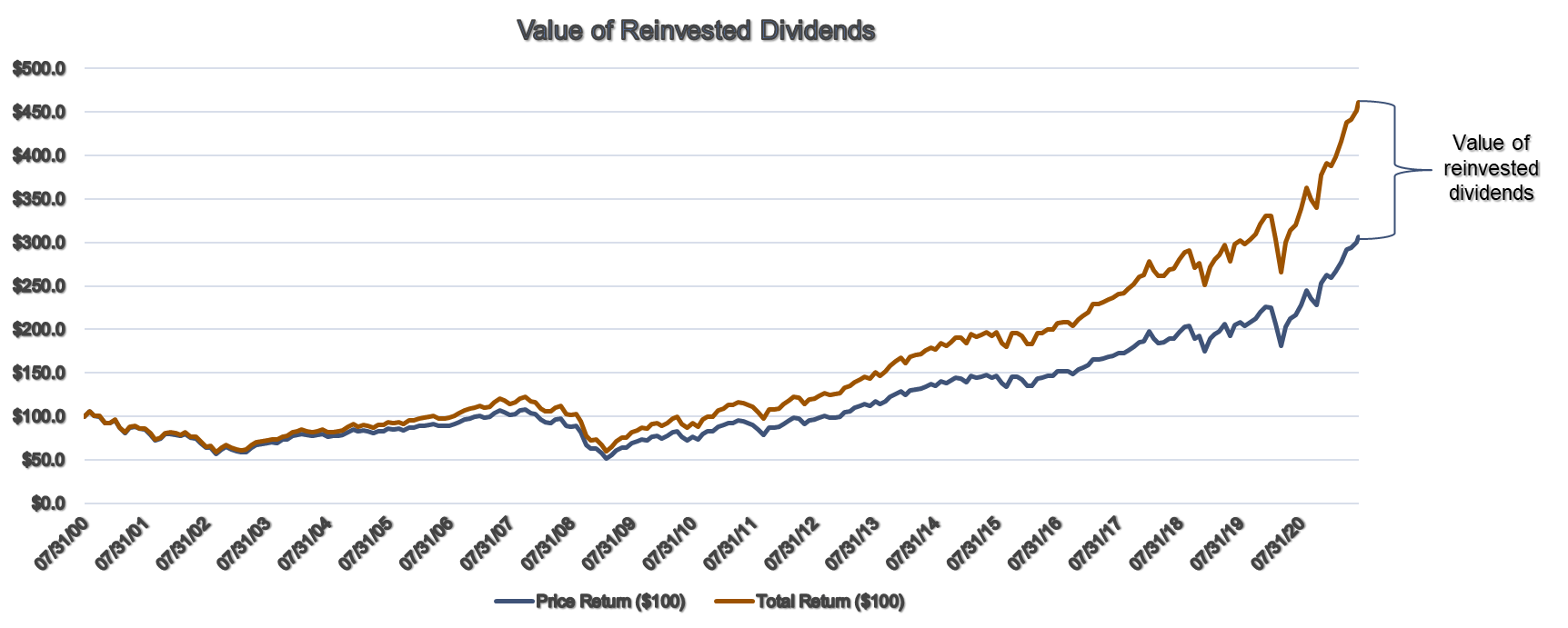

Since the beginning of the millennium, dividends reinvested into the S&P 500 are responsible for 33% of the total return (the other 67% is price appreciation). Dividends reinvested into the index produced a 372% total return (as of 8/25/21) vs a 214% return on the price of the index during the same time period.

Source: FactSet price history. S&P 500 index (1)

Let’s experiment with this concept of dividend vs price return across a 20-year time period for a retiree needing $30,000 annual income on a $1m portfolio. First, let’s set a few parameters for the experiment:

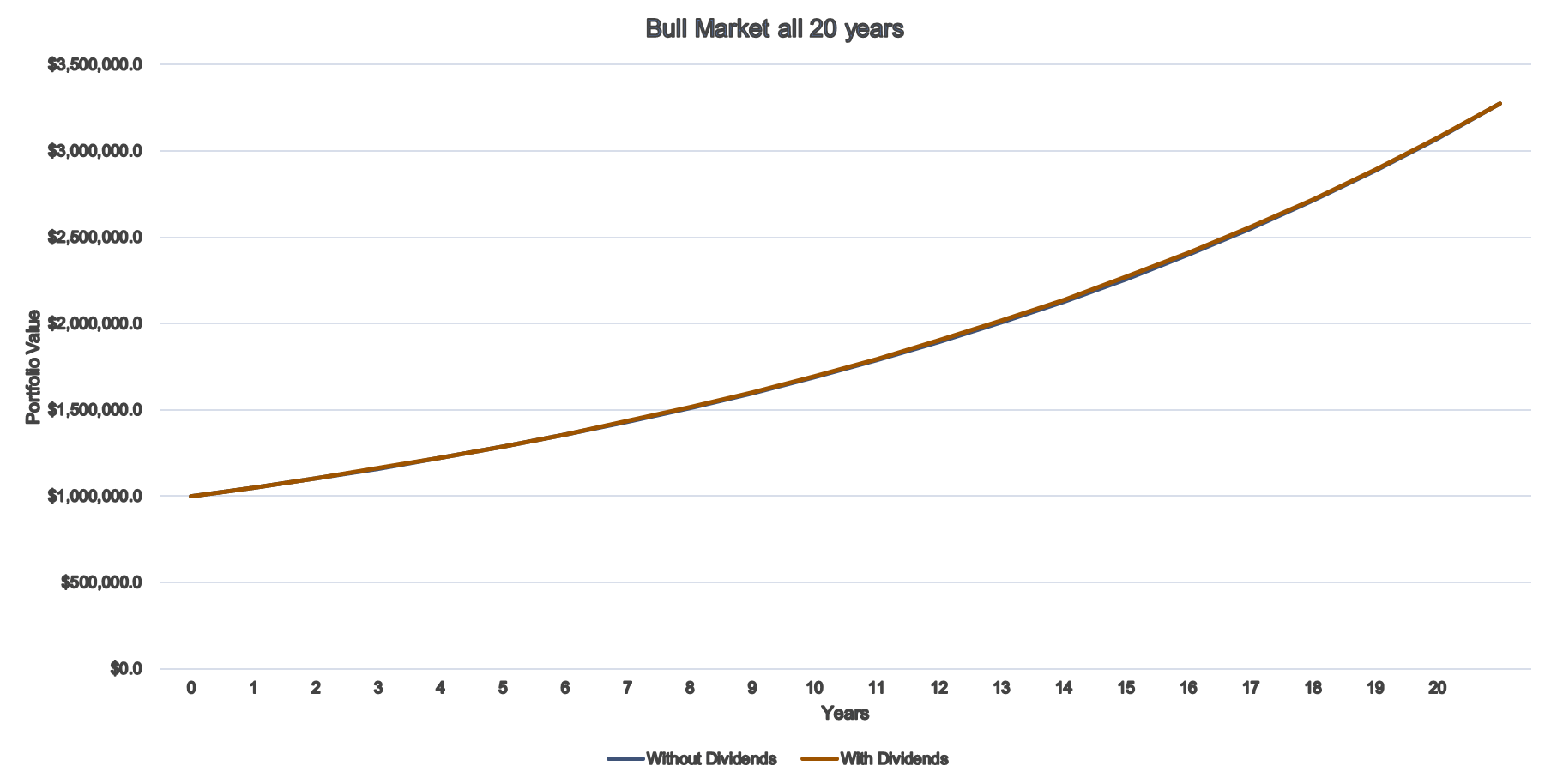

The retiree has two portfolio options:

Portfolio A does not produce income but has an 8% annual return.

Portfolio B produces a 3% current yield and a 5% annual return.

Portfolio B dividends are growing at 5.5% (to match the principal growth of portfolio A) and are never cut. Inflation is 2% annually and income needs must be met.

Because there are no dips in this 20-year time period, the returns of the two portfolios are equal. The dividend growth matches the principal growth of Portfolio A. A rational investor would be impartial to the portfolio selected under these conditions. This acts as our control.

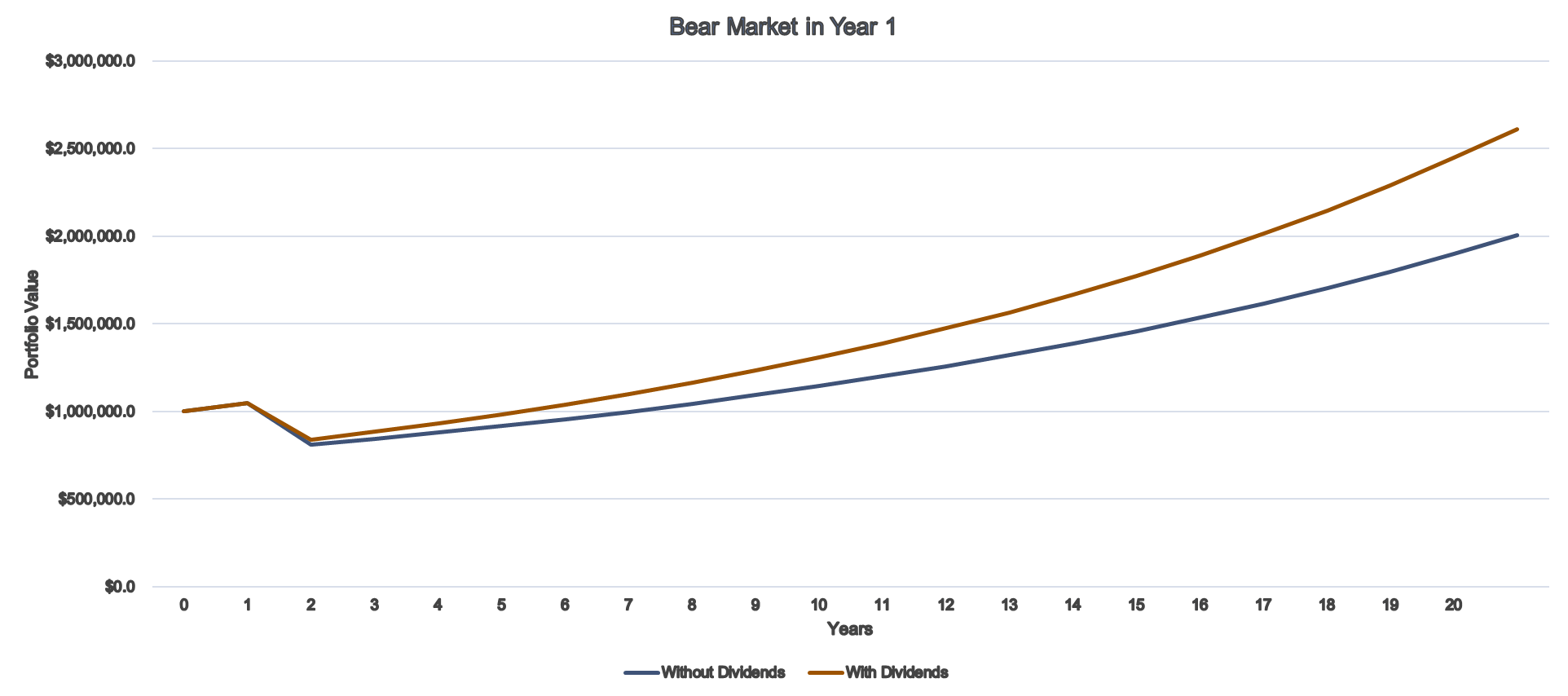

Now, imagine the same two portfolios get hit with the same -20% drawdown in year 1. In this case, the portfolio with the dividend option outperforms by about 30% cumulatively. Even though the principal shrinks in both cases, the dividends keep growing allowing the retiree to supplement their income needs. This is the “a bird in the hand is worth two in the bush,” effect. Because 3% of the return is cash-in-hand under this hypothetical scenario, portfolio B outperforms thanks to the dividend payouts that cover the withdrawal needs. In portfolio A, the investor withdraws $30,600 on top of the 20% loss. But in portfolio B, the withdrawal is covered by the dividend payouts making the principal withdrawal unnecessary. This accounts for the entire difference between the two portfolios.

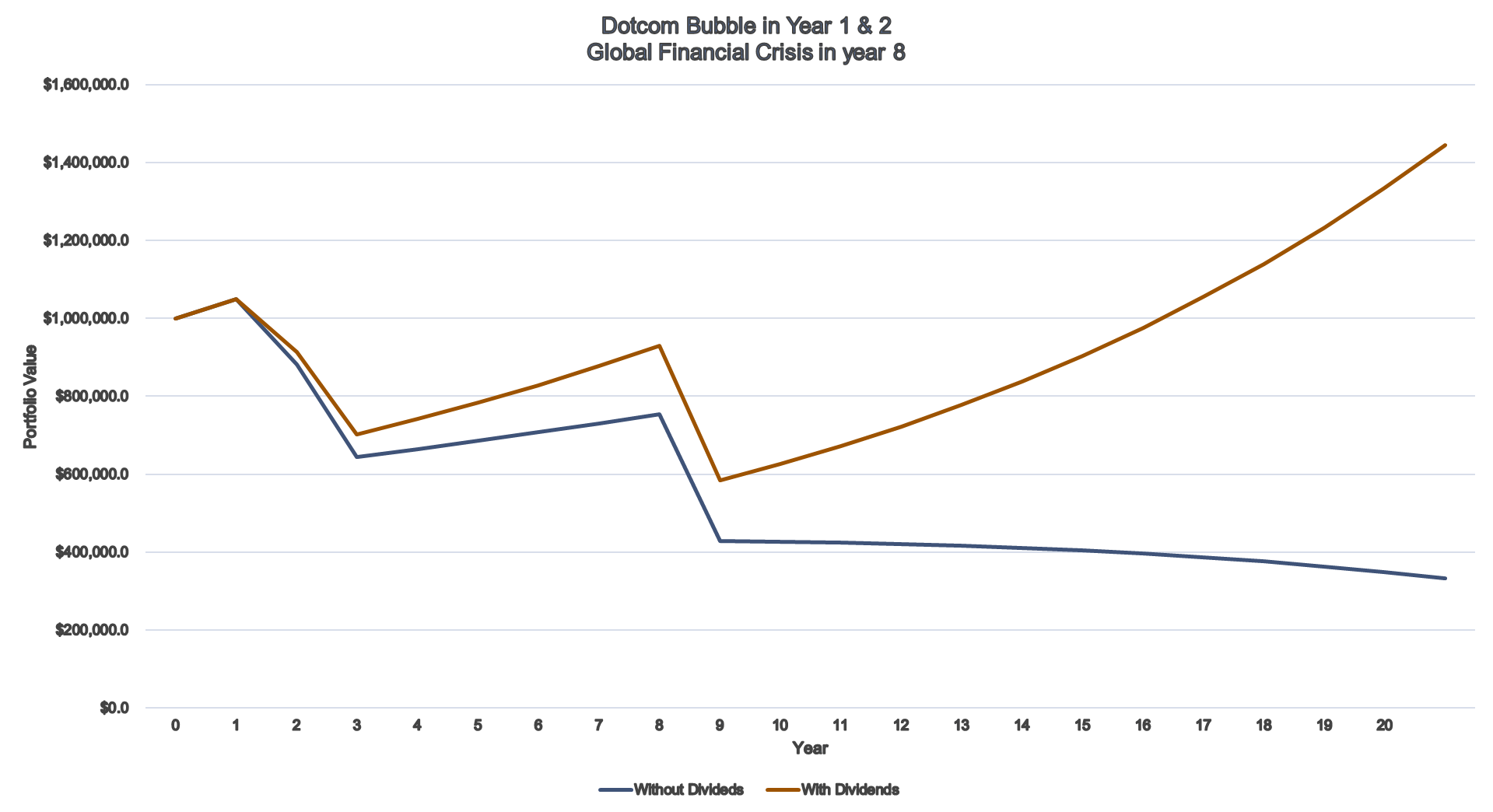

Now for the final, worst-case scenario. In this scenario, both portfolios are hit with the same declines seen in the Dotcom bubble in year 1 and 2 (-13.0% and -23.4%, respectively). Then the portfolios are hit again with a -38.5% decline in year 8 to simulate the Global Financial Crisis. In this case, the dividend portfolio recovers and continues to grow past the two black swan events. But, the portfolio without dividends never recovers. This is because the principal of the portfolio declined enough in year 8 that the withdrawal value (after accounting for inflation) exceeded the return value from year 9 on. In this year, withdrawals were over $35,000 but the 8% return on the smaller principal was only $34,000 so the net drawdown on the portfolio was ~-$1,000. In this case, the retiree would have to cut back on spending to allow the portfolio to grow again or run out of money.

Obviously, these are completely hypothetical scenarios. Stock prices, or dividends for that matter, never move in a linear fashion and neither are a guarantee. But, dividend reinvestment is a well-documented strategy for growing and protecting principal. Hopefully this appropriately demonstrates the power of dividend investing, specifically when it comes to retirees and principal protection.

If you want more information about how to utilize dividends in your portfolio, please visit our website at signaturewmg.com or reach out to us at 678-932-2500.

Brian Ransom, MBA, MS

Research Director

Signature Wealth Management Group

Sources:

- FactSet Research Systems. (n.d.). S&P 500 (Price History). Retrieved August 25, 2021, from FactSet Database.

This material is for informational or educational purposes only.

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

Diversification does not guarantee profit nor is it guaranteed to protect assets.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general

Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Please consult your financial advisor to discuss these strategies prior to implementation.